A Good Time for Lenders to Reevaluate Dividend Recaps

A Good Time for Lenders to Reevaluate Dividend Recaps

Receding Pandemic, Reviving Economy and Reality of Tax Increases…A Good Time for Lenders to Reevaluate Dividend Recaps

By Chuck Doyle, CTP, Founder, President and CEO, Business Capital

Today’s Market Creates Near Ideal Conditions

Over the last year or so, Washington has had a few pressing issues including the pandemic, election verifications and changing administrations. New priorities will be popping up and right or wrong, tax policy will take center stage. In that light, we thought we would highlight some items for lenders to think about as they recommend financing options for their clients as well as advise business owners on their option to take distributions out of their businesses. Being knowledgeable on this current topic can give lenders a leg up in helping their clients navigate upcoming tax changes by providing higher quality service and further cementing the relationship between business owner and lender.

A big movement is on the horizon in the Biden Administration’s proposed American Families Plan (AFP) regarding Long-Term Capital Gains (LTCG) and qualified dividend tax rates. Currently, the LTCG and qualified dividend rate is 20% and far lower than the current highest personal marginal tax rate (PMTR) at 37% – potentially 39.6% under the AFP. There is a reasonable chance the Biden Administration will be successful in adjusting the LTCG advantage and move to equal the highest PMTR for taxpayers with taxable income above $1 million. Just to bring that concept home, that is an 85% tax hike, potentially affecting a majority of business borrowers and lending relationships.

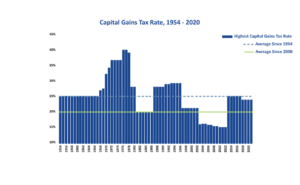

Capital gains tax rates, at just 20%, are far below the personal marginal tax rate of 37% and are likely to increase. Source: Tax Foundation. 2019-2021 estimated.

Further, there is talk of moving the PMTR up from 37% to 39.6%. In other words, it is quite conceivable that the LTCG will basically double in the foreseeable future and, when you add the additional 3.8% net investment income tax that would apply in this case, you’re looking at 43.4%!

On the lender side of the equation, the tax increase will dent bank earnings as much as $11 billion. Part of the Biden Administration’s proposals include a 15% minimum tax on book income, the pre-tax profits corporations report to investors. It’s targeted at very large corporations that pay little-to-no tax in some years.

Lenders have warned that this provision may have unintended consequences due to the vagaries of the mortgage market, where small lenders originate loans and then sell them to larger institutions that service them. They are proposing a bank-industry exemption for mortgage services stating they are not the intended target of the proposal.

Just to make things a little more interesting, conversations have included notions of tax rate increases being retroactive to earlier in the 2021 tax year. In fairness, we believe retroactivity is a remote possibility. That type of move generates profound economic uncertainty and sets a very disruptive precedent.

In dollar terms, this move results in a $2,000,000 added tax burden for each $10,000,000 of transaction value. Given transactions of size, that could add up to real money.

So how could this affect the conversation between lenders and their business owner clients? While selling an entire business is an option to avoid higher taxes on long term gains, that might not be the best solution to advise and could prove detrimental if they are planning on selling under the installment sale method, an approach which a majority of businesses transactions take. The installment sale method allows owners to spread the gain to subsequent tax years as they receive the principal payments from the buyer—sounds good until they realize they are now paying twice the amount of tax by picking up LTCG in subsequent years. If they are at all close to closing a transaction (or any stage for that matter) and have not discussed the option to opt-out of the installment sale, lenders should proactively have that conversation with the owner. Opting out places the full amount of the LTCG in the tax year of the sale. It would make more sense for the lender to suggest loan options that cover the initial tax hit and then have the borrower paydown the loan as they receive installment payments. This alone would be a far bigger savings than paying higher LTCG in subsequent years and would be a good insurance policy against the legislation passing.

“The installment sale method allows business owners to spread the gain from their sale to subsequent tax years as they receive principal payments from the buyer,” notes Chad McArthur, CPA with Hood & Strong LLP. “This sounds good until you realize you are now paying twice the amount of tax by picking up the LTCG in subsequent years.”

Lenders should consider discussing one of the many recapitalization scenarios that allow owners of medium- to large-sized companies to withdraw funds at the current LTCG rates while maintaining control of the business, since the owner(s) give up no equity. Dividend recaps are one such solution; in this scenario, the company takes on additional debt to fund a one-time cash dividend to shareholders.

Another scenario to reward shareholders is through a share repurchase program. A share repurchase program has the obvious benefit of potentially increasing EPS, cash flow per share and return on equity. Another benefit is profits on shares are taxed only when they are sold. However, if the company’s revenues falter after the buyback, the stock price will likely decline, providing a less attractive reward for shareholders.

Dividend recaps are being prompted by tax changes, but they are supported by four beneficial aspects of the current economy and factors intrinsic to a recap transaction.

These include:

- Historically low interest rates

- A strong economy

- Substantial bank liquidity

- Dividend recaps are typically done without an equity component

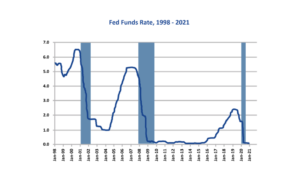

The federal funds rate is at near record lows and helps make strategies such as dividend recaps more attractive for lenders. Source: https://numbernonics.com/fed-funds-rate-2

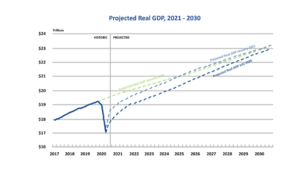

The Congressional Budget Office forecasts the U.S. economy to resume steady growth continuing to 2030, a healthy economy assists businesses in paying down debt taken on in a dividend recap.

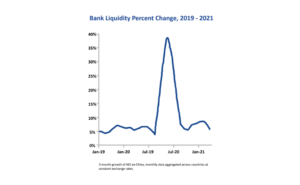

While bank liquidity is decreasing as stimulus injections end, cheap cash remains plentiful. Source: Reuters

Lenders should recommend owners consider dividend recaps as a viable option for companies that have a strong record of revenue growth and profitability, a strong market position and consistent cash flow, while arranging other forms of leverage for less stable companies if there are unencumbered assets.

Why Dividend Recaps Are A Solution Lenders Should Discuss with Clients

A healthy economy for most of the last decade has enabled many business owners to build successful, profitable businesses with little or no leverage. Interest rates remain at or near historic lows. Lenders are eager to find new areas for investment. These and other factors create an ideal situation for dividend recaps. Many capital providers consider dividend recaps as an option only for investment firms and larger corporations but in fact, they are a viable option for the owners of mid-sized private companies as a strategy to increase liquidity and diversify their assets.

Here is an example of a recent transaction. A B2B business owned by two principals had achieved an attractive inflection point. EBITDA was beginning to spike as the company had achieved economies of scale. In the prior fiscal year, EBITDA approximated $4MM but was on track to achieve roughly $8MM in the current fiscal year. At their lender’s urging, the company arranged for a $15MM cash flow term loan leaving a $6MM line of credit completely available for continued working capital requirements. Proceeds were used to fund a like size dividend. The owners achieved significant diversification of net worth and a competitively priced term loan. A growth focused lending community competed to provide attractive term sheets and the prognosis for the business remains strong supported by a resurging economy.

A win-win for both the capital provider and client.

The owners achieved their objective to withdraw cash from the business while maintaining ownership. They were able to secure cash without selling the business and postponed the need to sell the business. While the company’s debt level grew, the increase was well within acceptable debt capacity and provides clear runway for a solid long-term relationship with the lender.

But They Aren’t for Everyone

However, while dividend recaps offer owners several benefits in terms of diversifying the net worth and creating liquidity, there are potential risks for lenders to discuss with their clients. The most obvious is that a recap increases leverage without a commensurate increase in revenues or cash flow. If an economic downturn occurs while the company is paying down the debt, the company may become significantly weakened. Added debt may also preclude the company from pursuing new opportunities and/or constrain day-to-day working capital.

Lenders can provide value to their clients who own private businesses by pointing out the options that exist for taking cash out and, before embarking on a dividend recap or any type of leveraged recapitalization, help them evaluate carefully their financial goals, the health of their company and the broader economic climate to choose the financial solution that is the best fit.

Lenders hold the power to unlock opportunity within every business. Sometimes, traditional bank loans aren’t an option and selling the business outright is not in the best interest of ownership. They key to long-term success is exploring alternative funding approaches, such as dividend recaps.

About the Author

Chuck Doyle, CTP, is Founder, President and CEO of BizCap® (Business Capital since 2002). BizCap® delivers the best available cost of capital and industry leading structure to middle-market and lower middle-market companies seeking innovative financial strategies. The Company’s experience and long-standing network of high-level relationships with capital providers across a variety of disciplines allows the firm to efficiently deliver solutions for clients, particularly when they need immediate liquidity at a time when conventional sources of funding may be challenging or unobtainable.